Fraud Update: How Scammers Are Targeting Businesses

Fraud Update: How Scammers Are Targeting Businesses

Business fraud, illegal activity that takes your company's money and puts it into someone else's pocket, is a growing threat. The Association of Certified Fraud Examiners estimates that organizations lose about five percent of their gross revenues to fraud.1 Sometimes this fraud is committed by a random cyberthief; other times, by a customer, a vendor or even an employee.

Being aware of the types of fraud and how they are being perpetrated against companies can help you protect your own business. The following is information about some common types of fraud, along with precautions you can take to help keep your business safe.

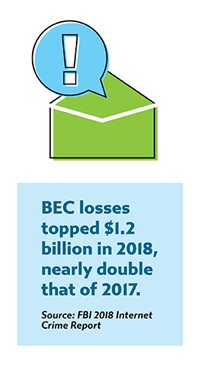

Business email compromise (BEC)

The threat:

BEC scams involve cybercriminals who compromise legitimate business email accounts to conduct unauthorized transfers of funds. These typically involve "spoof" emails, which appear to the recipient to come from a known source while they are actually counterfeit messages from a perpetrator.

For example:

For example:

- An email that appears to be coming from an established vendor may announce a change in payment instructions. When the employee recipient makes this change, they unwittingly redirect funds to an illegitimate account.

- A business leader's email may be spoofed so that it appears they are instructing an employee to initiate a wire transfer. The employee dutifully carries out the assignment only to discover later that those funds were directed to a fraudulent location.

- Employees may receive a "phishing" email, luring them to click on a link to a bogus website where they are asked for IDs, passwords or other sensitive information that provides the scammer with access to payroll or other internal records that enable them to tap into funds. Alternately, an employee's click on a nefarious link or attachment may enable the download of malicious software (malware) such as ransomware, viruses and spyware, which can compromise sensitive data, offer the scammer the means to extort the business or take down the entire IT system.

The scope, sophistication and frequency of BEC schemes continue to grow, so it's important to stay alert and be able to recognize a scam in the making.

What you can do:

Educate yourself and your employees about BEC and make a point of keeping up to date on the latest scams. Ongoing security education can help your employees recognize spoof emails and suspicious email requests. Put processes into place for verifying wire and payment requests before they are carried out. Also ensure that your systems are adequately protected by a firewall and antivirus technology, that employees are using strong passwords and that your team updates software security patches as soon as they become available.

Internal fraud

The threat:

The threat:

As much as you may not ever want to think your employees could be capable of committing crimes against your company, internal, or occupational fraud is a reality among businesses of all sizes. Companies with fewer than 100 employees are particularly vulnerable, says the Association of Certified Fraud Examiners, usually because business owners are unaware of this threat and because smaller companies may not have the resources to put adequate internal controls into place.

Occupational fraud may include any of a vast number of schemes. Asset misappropriation tops the list with activities such as cash theft, check tampering, payroll and billing schemes, etc. Employees may leverage their positions to build relationships with vendors or customers that put them closer to vulnerable information and processes, and when they collaborate with other employees, the potential for corporate losses grows. Data theft and bribery and corruption are common types of internal fraud as well.

What you can do:

Hire thoughtfully, including conducting a thorough background check on every candidate. Never put an individual employee in charge of an end-to-end process involving finance, and trust but verify: Internal controls, such as data monitoring/analysis and surprise audits may help you detect irregular activity early on.

It's also important to minimize temptations and add controls to protect your business accounts. For example, set spending limits on corporate credit cards and limit where they can be used. Monitor your bank accounts electronically for real-time transparency and take advantage of remote deposit capture, scanning and sending digital images to the bank rather than allowing paper checks to leave your office.

Most importantly, set the expectation of ethical behavior and nurture a culture of integrity.

Data breaches and other cyberattacks

The threat:

We hear a lot of news about cyberattacks (data breaches in particular) when huge corporations are involved, but cyberthieves attack businesses of all sizes. What's their intent? Stealing customer and other sensitive data, holding IT systems hostage until a specified payment is made (online extortion), infiltrating and damaging your computers and networks, etc.

What you can do:

Ensure that your systems are adequately protected by a strong firewall and antivirus technology and update software security patches as soon as they become available. Software-at-rest protection is available, too, as encryption tools render any stolen data useless to the perpetrator. Consulting with a technology security expert about the potential need for vulnerability scanning, which will identify any weaknesses in your system, is prudent as well.

Click here for a downloadable whitepaper copy of this post.

Our treasury management experts are here to help. If you'd like to discuss solutions for your business, call 1-855-282-3888, Monday - Friday from 8:30 AM - 5:00 PM.

1Report to the Nations: 2018 Global Study on Occupational Fraud and Abuse, Association of Certified Fraud Examiners

This article is for general information purposes only and is not intended to provide legal, tax, accounting or financial advice. Any reliance on the information herein is solely and exclusively at your own risk and you are urged to do your own independent research. To the extent information herein references an outside resource or Internet site, Dollar Bank is not responsible for information, products or services obtained from outside sources and Dollar Bank will not be liable for any damages that may result from your access to outside resources. As always, please consult your own counsel, accountant, or other advisor regarding your specific situation.

Posted: September 11, 2020

The right financing can help your business seize opportunities that might otherwise be out of reach. Learn how to evaluate borrowing decisions, maintain healthy cash flow and choose the loan or line of credit that aligns with your company’s needs. With a thoughtful approach, business debt can be a powerful tool for growth.

If you’re a business owner, deciding when and how you will pass on or sell your company should be an intentional decision. Starting at the end means thinking about what you want to gain at the time of your exit.

Whether your company serves customers in person or online, it is important to provide a variety of quick, easy and secure payment options to make it as easy as possible for customers to do business with you.

If you have ever struggled to meet the everyday expenses of your company, then you know all too well the value of effectively managing your working capital. This article explains why working capital is so important to your company and offers ideas for increasing your cash stash.

Enterprising business leaders welcome the opportunity to develop innovative solutions that help their companies become more successful and resilient. But where do you start to effectively master the art of creatively leveraging the resources at hand to give your company an edge? These ideas may help.